A real estate investment trust (REIT) lets you invest in income-producing real estate through shares, without owning property directly. REITs generate returns through dividends and price growth, making them a popular option for passive income and portfolio diversification.

A real estate investment trust, as a unique asset class, lets you invest in property without buying a building yourself, and that’s why so many people use REITs for income, growth, capital appreciation, and portfolio diversification.

With search interest in REITs on the rise, the main challenge is picking one that fits your specific financial goals. Some investors want steady dividends, others want long-term growth, and many want both without the headache of managing tenants or repairs.

REITs can give you that mix, but the right move still depends on what you buy, how it’s priced, and how it fits inside your portfolio. The key is to start with the basics, compare the options with clear numbers, and invest with a plan instead of a guess.

Key Takeaways

- A real estate investment trust: A REIT lets you invest in income-producing real estate without buying or managing property yourself.

- REITs must pay out at least 90% of taxable income as dividends in the U.S., which makes income coverage an important screening point.

- Equity REITs own properties, while mortgage REITs lend against real estate, and the two carry different risk profiles.

- FFO and AFFO are more useful than net income for judging whether a REIT can support its dividend.

- A REIT ETF is often the simplest first step if you want diversification and less single-company risk.

What a REIT Is, and What You Are Really Buying

A real estate investment trust, which requires SEC registration, sounds formal, but the idea is simple. You are buying a slice of a company that owns or finances income-producing property, then shares the cash flow with investors.

That matters because the investment is not the same as owning a house or apartment building outright. You are buying shares in a business, and that business is tied to real estate.

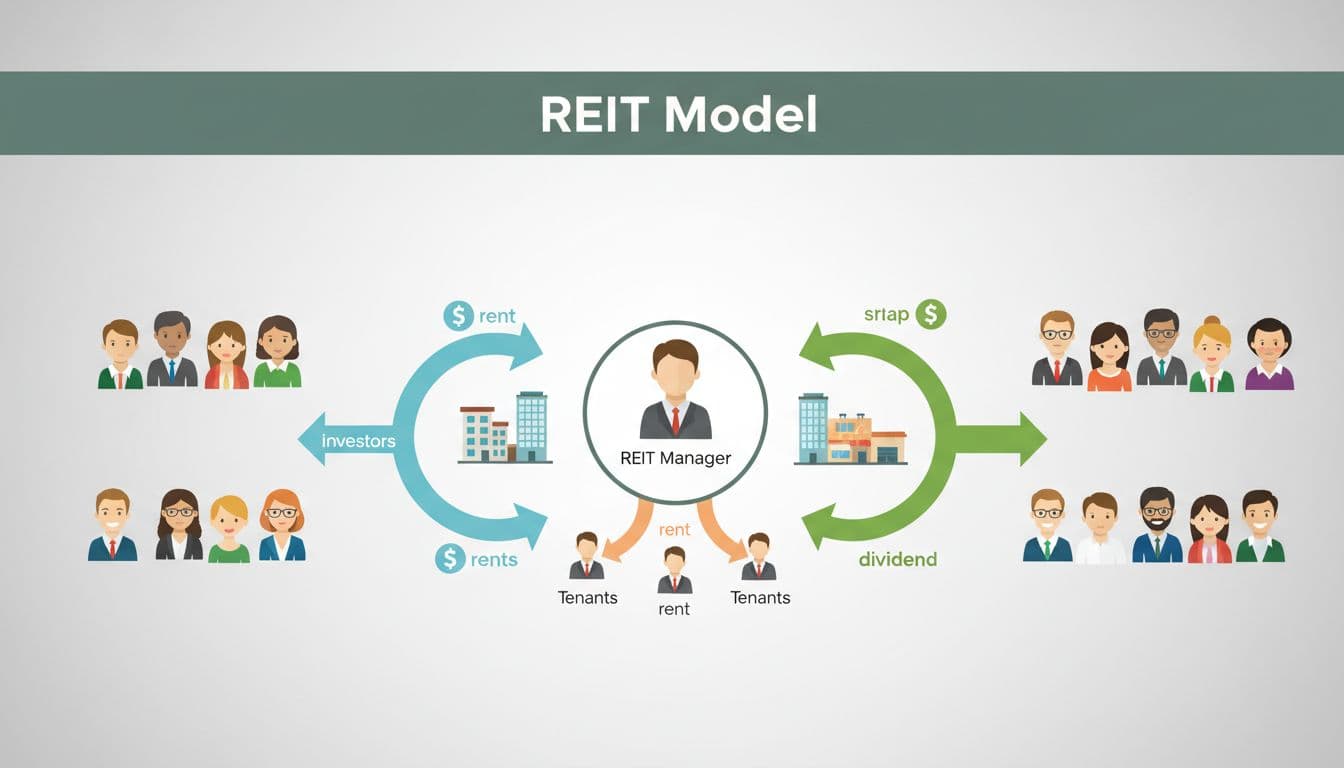

The basic REIT business model

A REIT pulls money from investors by selling shares. The REIT then uses that capital to buy properties, fund mortgages, or both, depending on the type of REIT.

Here’s the flow in plain language:

- Investors buy shares

- Your money goes into the REIT, much like buying stock.

- The REIT buys or finances property

- It may own apartments, warehouses, offices, storage units, or other income-producing real estate.

- The properties generate cash

- Tenants pay rent, or borrowers pay interest.

- The REIT sends income back to shareholders

- That payout usually comes as shareholder dividends.

The key rule beginners need to know is the 90% payout rule. In the U.S., a REIT must pay out at least 90% of its taxable income to shareholders, per the Internal Revenue Code, to keep its REIT status. In simple terms, that rule pushes most of the income back to investors instead of keeping it inside the company.

According to the U.S. Securities and Exchange Commission, REITs must distribute at least 90% of taxable income to shareholders to maintain their tax-advantaged status, which is why they are widely used for income-focused investing.

A Real Estate Investment Trust is built to collect real estate cash flow and pass most of it along to shareholders.

That is why many REITs are popular with income-focused investors. For a plain-English breakdown of how REITs work, the SEC’s REIT investor alert is a useful reference.

REITs versus owning rental property yourself

Buying REIT shares is very different from buying a rental property. With a REIT, you can start with less money, avoid repairs, and get in or out more easily because shares trade like stocks.

Direct ownership gives you more control, but it also gives you more work. You choose the property, screen tenants, handle maintenance, track expenses, and deal with vacancies. That can be rewarding, but it takes time and cash.

REIT investing usually gives you:

- Lower cost to start: You can buy shares without a large down payment.

- Less day-to-day work: No late-night repair calls or lease renewals.

- Better liquidity: Public REITs are easier to sell than a building.

- Less control: You do not pick tenants or decide when the roof gets replaced.

Direct rental ownership gives you the opposite mix. You get more control, but you also take on more responsibility and more hassle. If you want a side-by-side comparison, Investopedia’s REIT vs. direct real estate overview lays out the tradeoffs clearly.

That tradeoff is the heart of real estate investment trust how to invest decisions. You are not buying a building, and you are not becoming a landlord. You are buying a stake in a real estate business that turns property income into shareholder payouts.

The main REIT types you should know before you buy

Before you buy your first REIT, it helps to know that they do not all work the same way. Some own buildings and collect rent. Others make money from loans tied to real estate. A few trade on stock exchanges, while others stay private and less liquid.

That mix matters because the type you choose changes your income, risk, and how much your investment may swing. If you’re learning real estate investment trust how to invest, start with the structure first, then compare the property focus. A REIT that owns apartments will not behave like one that funds mortgages or one that holds data centers.

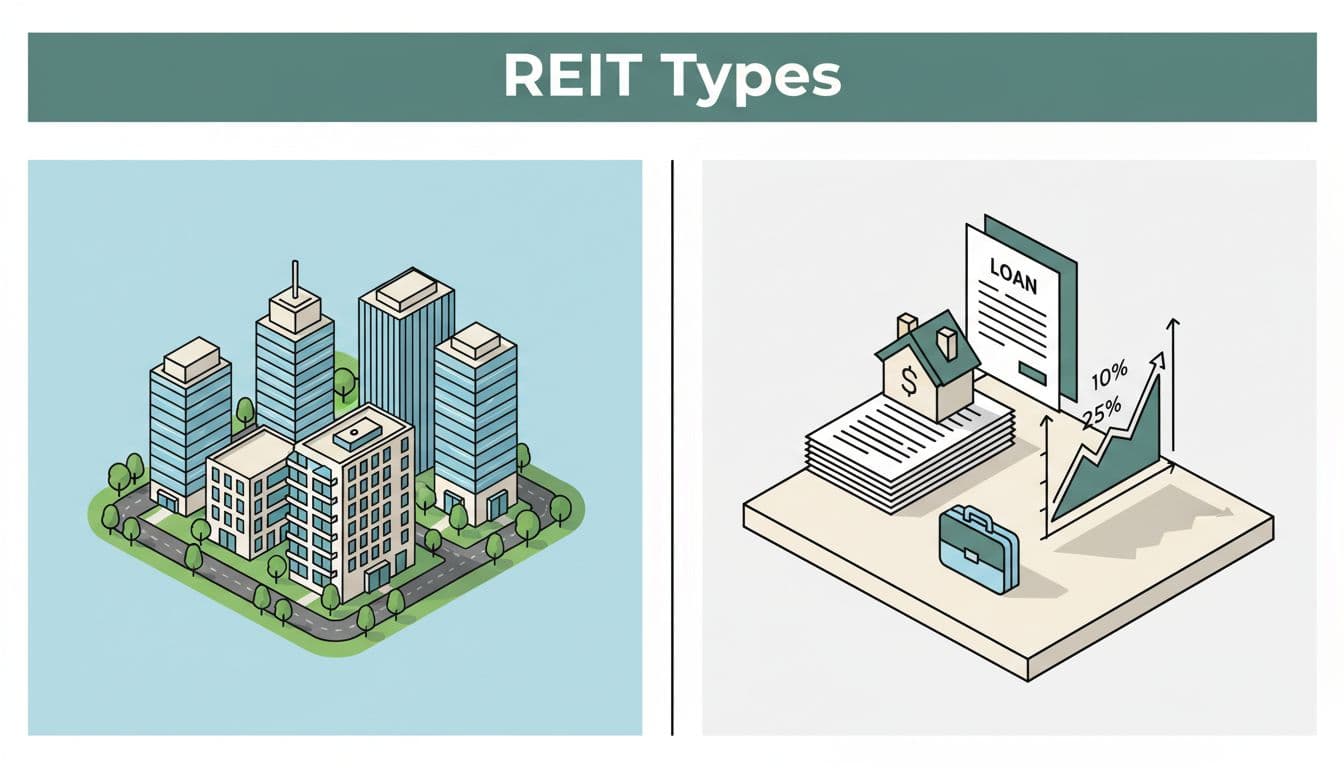

Equity REITs, the most common starting point

Equity REITs own real estate, then earn money from rent and property sales. These are the REITs most beginners hear about first, and for good reason. They are easy to understand, and their income comes from assets most people recognize, like apartments, warehouses, malls, offices, and other commercial real estate.

They also give you a direct link to property performance. If tenants stay, rents rise, and vacancies stay low, the REIT usually has a better shot at steady cash flow. Still, the property type matters a lot. An apartment REIT may benefit from strong housing demand, while an office REIT can face pressure if companies cut space.

That is why many investors start here. Equity REITs are simple on the surface, but they still give you room to choose between growth, income, and sector exposure. For a broader look at how these sectors differ, Nareit’s REIT types overview is a solid reference.

If you want a clean first step, equity REITs usually give the clearest picture of how real estate income works.

Mortgage REITs, and why they behave differently

Mortgage REITs, often called mREITs, do not own buildings in the usual sense. They make money by lending against real estate or by buying mortgage-backed securities. In simple terms, they are closer to lenders than landlords.

That business model can produce higher income, but it also comes with more rate risk. When interest rates move, mortgage REITs can feel the change fast because their borrowing costs, loan values, and spreads all shift. As a result, these REITs often swing more than equity REITs.

They can fit an income-focused strategy, but they need closer attention. If you’re comparing payouts, ask where the cash comes from and how stable it looks across rate cycles. The S&P DJI guide to REIT sectors explains the split between equity and mortgage REITs in a clear way.

Public, private, and sector-based REIT choices

REITs also differ by how you buy them. Publicly traded REITs list shares on stock exchanges, so you can buy or sell during market hours. Non-traded REITs and private REITs do not trade that way, which means they usually have less liquidity and can be harder to exit.

That difference matters if you want flexibility. Publicly traded REITs are easier to price and move in and out of, but they can also react quickly to market fear. Non-traded REITs and private REITs may feel calmer day to day, yet your money may be locked up longer.

Sector focus adds another layer. Apartments, industrial properties, retail centers, and data centers all respond to different economic forces. Apartments often track housing demand. Industrial REITs benefit from e-commerce and logistics. Retail REITs depend on tenant quality and consumer traffic. Data centers can grow fast when cloud and AI demand stay strong, but they also need heavy power and capital spending.

A quick comparison helps:

| REIT type | Main income source | Typical risk profile |

|---|---|---|

| Public REITs | Rent or mortgage income | Easier to trade, more market swings |

| Private REITs | Rent or mortgage income | Less liquid, harder to exit |

| Apartment REITs | Residential rent | Sensitive to occupancy and new supply |

| Industrial REITs | Warehouse and logistics rent | Often steadier, tied to shipping and e-commerce |

| Retail REITs | Store rent | Depends on tenant strength and consumer demand |

| Data center REITs | Server and storage space rent | Growth-driven, but capital-heavy |

The main takeaway is simple. The REIT label alone does not tell you enough. You need to know whether the REIT owns property, lends money, trades publicly, or focuses on a sector with its own risks and rewards. That is the difference between picking a ticker and picking a fit for your portfolio.

How to invest in REITs step by step

Investing in REITs involves choosing your goal, analyzing cash flow metrics, selecting a REIT or ETF, and buying through a brokerage accoun

Buying a real estate investment trust is a straightforward process once you know the sequence. To keep it simple, follow these steps to move from setting your strategy to executing your first trade.

- Define your goal: Decide if you are seeking long-term growth, immediate dividend income, or a blend of both.

- Research the fundamentals: Use metrics like FFO and AFFO to ensure the real estate investment trust has stable, sustainable cash flow.

- Select your vehicle: Choose between an individual real estate investment trust for specific exposure or an ETF for instant diversification.

- Execute the trade: Use a low-fee brokerage account to place your buy order once you have vetted the asset.

Set your goal before you pick a REIT

Start with the reason you want to invest. Some people want steady income from shareholder dividends. Others want long-term growth and can live with bigger price swings. Many investors want a mix of both.

Your time horizon changes the answer. If you may need the money soon, a REIT with a shaky dividend or a volatile share price can be a poor fit. If you can hold for years, you can usually tolerate more ups and downs.

Risk tolerance matters too. A utility-like income REIT may feel calmer than a niche sector tied to tech or office demand. Still, even a “safer” REIT can fall when rates rise or the market turns cautious.

Before you buy, ask yourself three simple questions:

- What do I want this money to do? Income, growth, or both.

- How long can I stay invested? Months, years, or longer.

- Will I need this cash soon? If yes, keep your position smaller or wait.

If you may need the cash in the next few years, focus on stability first, not yield alone.

Research the REIT the smart way

Once you know your goal, look at what the REIT actually owns. Apartments, warehouses, hospitals, data centers, and retail centers all behave differently. Tenant quality matters too, because strong tenants usually mean more reliable rent.

Debt is another big one. A REIT with too much debt can get squeezed when interest rates rise. You don’t need to become an analyst, but you do need to know whether the balance sheet looks manageable.

Dividend history helps, but don’t stop there. A high payout can look attractive and still be fragile. Check whether the dividend has been steady, raised over time, or cut in past downturns.

Two key metrics can help you judge the payout:

- FFO, or funds from operations: a better measure of REIT cash flow than regular earnings.

- AFFO, or adjusted funds from operations: a more refined version that tries to show what is left after recurring costs.

If those terms feel fuzzy, the main idea is simple. They help show whether the REIT has enough real cash flow to support its dividend. The Investor.gov REIT guide is a good place to review the basics, and this FFO and AFFO overview explains the metrics in plain language.

Open a brokerage account and place your first trade

To buy a public REIT, REIT exchange-traded fund, or mutual fund through a brokerage account, you need a brokerage account. Look for one with low fees, no account minimum, and research tools that make it easy to compare options. In the U.S., platforms like Charles Schwab, Fidelity, Robinhood, and Vanguard are common starting points because they offer $0 stock and ETF commissions.

The best fit depends on how you invest. Schwab and Fidelity are strong if you want research tools. Vanguard works well if you plan to buy low-cost ETFs and hold them. Robinhood is simple if you want a clean mobile app and small starter purchases.

The trade itself is straightforward. After you fund the account, search for the REIT ticker or ETF symbol, choose the number of shares, then place a buy order. A market order buys at the current price, while a limit order lets you set the highest price you’re willing to pay.

A clean first trade often looks like this:

- Open and fund the brokerage account.

- Search for the REIT or REIT ETF ticker.

- Review the current price and fee details.

- Choose a market or limit order.

- Confirm the trade.

Start small if you need to. A first trade should teach you how the process works, not force you to bet big on day one.

Why a REIT ETF can be a safer first move

If picking one REIT feels like too much, a REIT ETF can make the first step easier. An ETF holds many REITs inside one fund, so your money is spread across several companies and property types at once, much like the diversification offered by the S&P 500.

That spread helps lower single-company risk. If one REIT cuts its dividend or runs into trouble, the whole position does not rely on that one name. It also gives you broad exposure without forcing you to pick the “winner” in one sector.

For beginners, that can be a cleaner starting point. You still get access to real estate income and price growth, but with less pressure to analyze every balance sheet right away. If you want a broad, low-cost entry point, a fund like this can fit well inside a long-term portfolio.

A REIT ETF is often a good first move when you want:

- Simple diversification across many REITs.

- Lower company-specific risk than buying one stock.

- An easier way to start with less research and fewer decisions.

That makes ETFs useful for new investors, and it also makes them practical for anyone who wants real estate exposure without spending hours sorting through individual names.

How to judge whether a REIT is worth your money

A REIT can look attractive on paper, but the real test is simple: does the income hold up, and does the business stay healthy when conditions change? A big dividend alone does not answer that.

When you’re learning real estate investment trust how to invest, focus on the parts that support the payout. Cash flow, debt, tenants, and return numbers tell you a lot more than a headline yield.

Look past the dividend yield

High dividend yields can be a warning sign. Sometimes the market pushes the price down because investors expect trouble ahead, and that can make the yield look larger than it really is.

What matters is whether the dividend comes from real cash flow. A REIT with strong properties, stable tenants, and enough funds from operations can usually support its payout better than one chasing attention with a big number.

A yield looks good only when the business behind it looks good too.

You should also ask how the dividend compares with the REIT’s cash flow. If most of the cash is already spoken for, the payout can be fragile. That is why REIT investors often look at FFO and AFFO, not just net income. For a clear breakdown of those measures, this REIT valuation guide is a solid reference.

A practical check looks like this:

- Stable or rising FFO means the REIT is generating real operating cash.

- AFFO that covers the dividend gives the payout more room to breathe.

- A cut in the dividend history can point to stress, even if the current yield looks tempting.

In other words, a 7% yield with weak coverage can be worse than a 4% yield backed by strong cash flow.

Check debt, occupancy, and tenant quality

Debt matters because REITs often borrow to acquire properties.

Too much leverage increases risk when interest rates rise.

Strong balance sheets provide more flexibility during downturns.

Occupancy is just as important. Empty space does not pay rent, so lower occupancy means less income. If a mall, apartment complex, or warehouse sits half full, the cash flow gets squeezed fast.

Tenant quality also makes a difference. A REIT with strong tenants, like national retailers or major service companies, often has steadier rent collections than one tied to weak or unstable tenants. For a useful checklist of REIT metrics, AAII’s fundamental analysis guide is worth a look.

A simple example helps. If two REITs both pay 5%, but one has heavy debt, weak occupancy, and shaky tenants, that higher yield may be compensation for more risk. The better deal is often the one with the cleaner balance sheet and steadier rent stream.

Use return numbers to compare deals

Return math keeps the decision grounded. ROI shows how much you make compared with what you put in. Cash flow tells you how much income you actually receive. IRR adds time into the picture, so it helps compare one REIT or property against another. Institutional investors also factor in market capitalization to assess scale and stability relative to these returns.

That sounds technical, but the idea is simple. A REIT that pays a steady dividend and grows over time may beat one with a flashy yield but weak long-term returns.

Use these three questions to compare opportunities:

- What is the expected ROI?

This tells you the rough return against your initial cost. - How much cash flow will I get each year?

This matters if you want income you can spend or reinvest. - What is the IRR over time?

This helps you compare a slower, steadier REIT with a faster-growing one.

If you want a deeper look at REIT screening, The Motley Fool’s REIT valuation guide explains why payout coverage and debt ratios matter so much. The best choice is usually the one that gives you solid cash flow without forcing you to take on hidden risk.

The biggest risks to watch before you invest in REITs

REITs can pay strong income, but they still come with real risks. The two biggest ones for most investors are interest rates and property market weakness. Both can hit REIT prices, dividend safety, and long-term returns.

If you’re learning real estate investment trust how to invest, don’t stop at the yield. A REIT can look attractive on the surface and still face pressure under the hood. The right move is to understand what can hurt it before you buy.

Why interest rates can move REIT prices

Higher interest rates usually put pressure on REITs for two simple reasons. First, borrowing gets more expensive. Second, income from safer fixed-income options starts to look better.

That matters because REITs often use debt to buy and improve properties. Publicly traded REITs, through SEC registration, disclose their debt structures clearly, which helps investors assess vulnerability. When rates rise, refinancing costs can climb, and that can leave less cash for dividends or growth. At the same time, investors may shift money into Treasury bonds or CDs because those choices feel safer.

Nareit explains that publicly traded REITs share prices often react to changes in rate expectations, especially long-term rates. Non-traded REITs may show different price sensitivities since valuations occur less frequently. You can see that effect clearly when bond yields move up and REIT prices soften. The Nareit guide on REITs and interest rates is a helpful read if you want the mechanics in plain language.

Here is the simple version:

- Higher borrowing costs can squeeze profits.

- Lower property values can hurt share prices.

- Stronger bond yields can pull income investors away from REITs.

When rate-sensitive assets compete with safer fixed income, REITs need stronger cash flow to stay appealing.

That does not mean every REIT falls every time rates rise. Some have fixed-rate debt and long lease terms that soften the blow. Still, rate risk is one of the first things to check before you buy.

How bad property markets can hurt returns

REITs depend on property income, so weak real estate markets can cut straight into returns from underlying real estate assets. Falling rents, empty units, and slower tenant demand all reduce cash flow. When that happens, dividends can grow more slowly, stall, or get cut.

The pressure can show up in a few ways. Occupancy may slip if tenants leave and new ones are hard to find. Rent growth can slow if landlords have to offer discounts or better terms to keep spaces filled. In a worse market, some tenants may default, which adds more strain.

This risk changes by sector. Apartment and hotel REITs usually feel downturns faster because leases reset often and demand can change quickly. Industrial and net-lease REITs often hold up better because they tend to use longer leases and creditworthy tenants. Data center and infrastructure REITs can also be steadier, although they still face their own capital and demand risks.

A quick comparison makes the difference clearer:

| Sector | Downturn effect | Why it matters |

|---|---|---|

| Apartments | Faster rent changes and occupancy swings | New supply or weaker demand can hit income quickly |

| Hotels | Immediate drop in bookings | Revenue resets daily, so weak travel demand shows up fast |

| Retail | Tenant stress and vacancy risk | Store closures can leave large spaces empty |

| Industrial | Often more stable | Long leases and logistics demand can support cash flow |

| Data centers | Mixed, but often stronger demand | Growth can stay solid, though costs are high |

The main point is simple. A weak property market does not hurt every REIT the same way. If you want a steadier path, check how the sector handled past downturns and how much of the REIT’s income depends on short-term demand.

A REIT with strong tenants, healthy occupancy, and a property type that holds up in slower markets has a better chance of protecting your income. That is the kind of detail that matters when you’re choosing a REIT, not just the yield on the screen.

Frequently Asked Questions About Real Estate Investment Trust (REIT)

What is a real estate investment trust (REIT)?

A REIT is a company that owns, operates, or finances income-producing real estate, allowing investors to buy shares for exposure to property cash flow without direct ownership. It must distribute at least 90% of taxable income as dividends to maintain its tax status. This model turns rent or interest into shareholder payouts, traded like stocks for easy access.

What’s the difference between equity REITs and mortgage REITs?

Equity REITs own and manage properties like apartments or warehouses, earning from rent and sales for more direct real estate ties. Mortgage REITs (mREITs) focus on loans or mortgage-backed securities, generating higher yields but with greater sensitivity to interest rate changes. Equity offers steadier property performance; mortgage brings more volatility and rate risk.

How do I start investing in REITs?

Set your goals for income, growth, or both, then research REITs using metrics like FFO, AFFO, debt, and occupancy. Open a low-fee brokerage account (e.g., Vanguard, Fidelity), search for public REITs or ETFs, and place a buy order—start small or with an ETF for diversification. Consider your timeline and risks before trading.

What metrics should I use to evaluate a REIT?

A good REIT shows strong cash flow, manageable debt, stable occupancy, and reliable dividend coverage—not just a high yield. Look beyond dividend yield to FFO and AFFO for true cash flow coverage, plus debt levels, occupancy rates, and tenant quality to gauge stability. High yields can signal risks if unsupported by strong operations.

What are the main risks of investing in REITs?

The biggest risks in REIT investing are rising interest rates and weak property markets, both of which can reduce income and push share prices down. Risks vary by sector—e.g., offices suffer more than industrials—and type, with mortgage REITs more rate-sensitive. Check historical performance and fixed-rate debt for resilience.

Conclusion

A real estate investment trust can be a simple way to own a piece of real estate without buying property yourself, offering a path to shareholder dividends. The best results usually come when you start with a clear goal, then compare the REIT’s income, debt, and property type before you buy.

Note that shareholder dividends are often taxed as ordinary income, so factor that into your planning.

That matters even more in a market where REIT prices can move with rates and sector trends. If you stay focused on cash flow, dividend coverage, and your own timeline, the choice gets much easier.

Before you place a trade, run the numbers and see how the return lines up with your plan. The FREE Real Estate Investment Returns Calculator on CalcLabAI is a quick way to model your capital appreciation and income targets for expected returns and a smarter move.

By Admin

Published: April 29, 2026

Last Updated: April 29, 2026

Disclaimer: This content is for informational purposes only and should not be considered financial or investment advice. Always consult a licensed financial advisor before making investment decisions. Real estate investments, including REITs, involve risk and may result in loss of capital.